What Does Mortgage Investment Corporation Mean?

Table of ContentsWhat Does Mortgage Investment Corporation Do?The Greatest Guide To Mortgage Investment CorporationThe 8-Minute Rule for Mortgage Investment CorporationMortgage Investment Corporation Can Be Fun For AnyoneThe 7-Second Trick For Mortgage Investment Corporation

If you intend to be a component of this industry and have the financial investment to do so, think about becoming a stakeholder in a home loan financial investment company. Buying a trustworthy MIC, like Metropointe Home loan gives you a trusted stream of revenue. Assist enhance payments Mark contributions as purposeless if you find them irrelevant or otherwise important to the article.

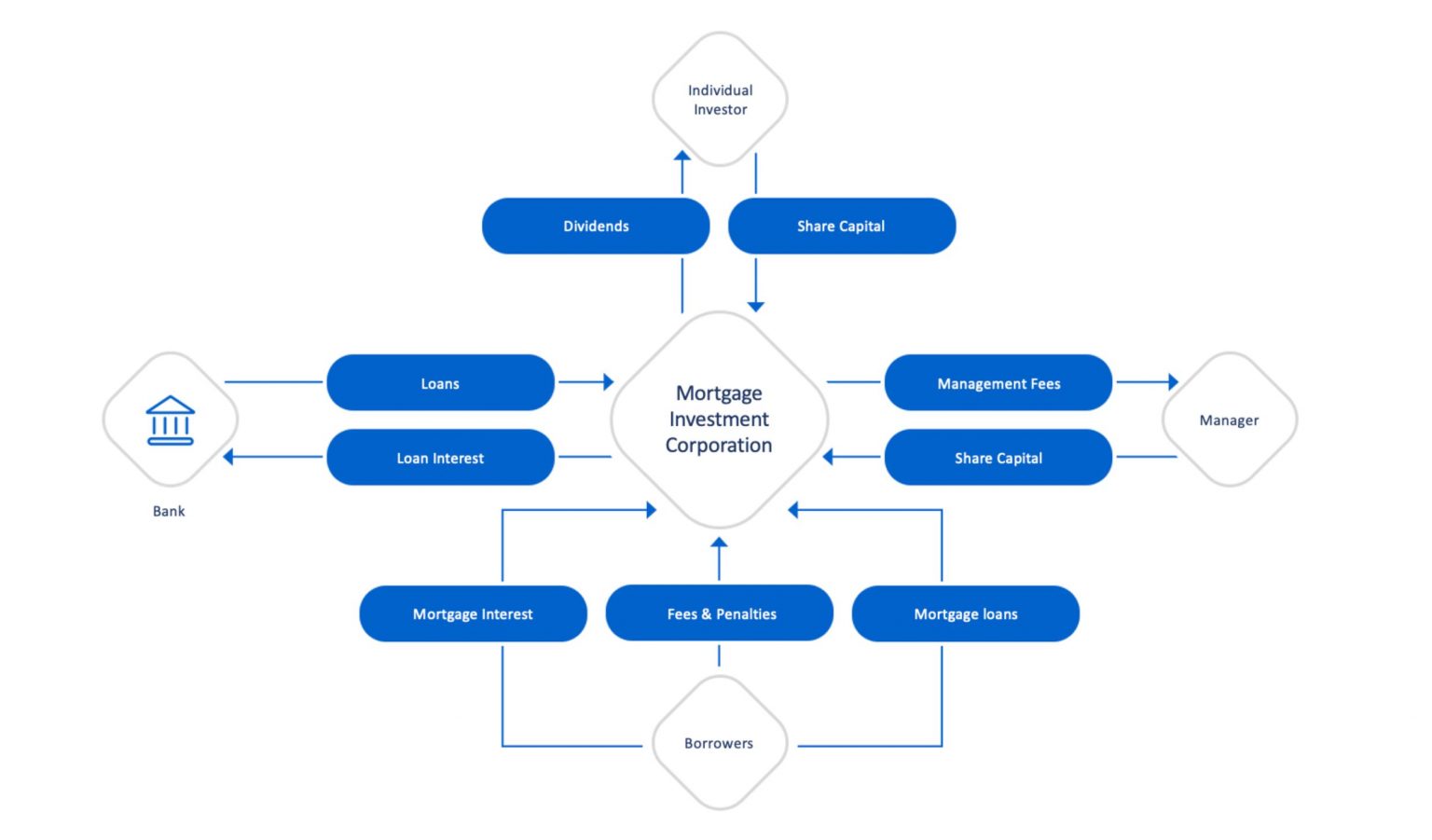

A Home Loan Financial Investment Corporation (MIC) is an investment fund where financiers merge their cash to lend to debtors as exclusive mortgages. By adding their cash to this swimming pool, a capitalist purchases shares in a MIC.

This combination of investor funds and small business loan is after that offered by the MIC to consumers subsequently. Collectively, the contracts of these borrowers to pay back the MIC, together with the genuine estate that works as these arrangements' collateral, compose the MIC's home loan profile. When the debtors make their mortgage settlements, any kind of linked costs and interest are cycled back into the fund.

MICs are subject to regulative demands and oversight, making certain compliance with safety and securities regulations and capitalist defense. In Canada, MICs have actually been generally used genuine estate investment because 1985, when they were produced as an outcome of Area 130.1 of the Earnings Tax Act. This federal statute permits capitalists to spend in a swimming pool of home mortgages.

The Only Guide for Mortgage Investment Corporation

A Mortgage Financial Investment Company (MIC) is a mutual fund that pools resources from financiers to offer debtors in the type of exclusive home loans. This method to investing rises the flow of cash offered for the MIC to money home loans in the realty market and just as offers a means for investors to take part in the property real estate market while reducing the moment and risk of buying specific home loans.

A MIC functions as a form of guard to investors from the danger of private lending and is not as capital intensive as funding home loans as a specific capitalist. Procedures of Mortgage Financial investment Corporations are performed by the MICs management. These operations include sourcing home loan financial investments, evaluating applications for mortgages, settlement of relevant interest prices, and basic management.

You have actually probably never heard of a Home loan Investment Company (MIC) as an investment. A couple of months back, the topic of Home loan Investment Firms (MIC) was brought to our attention.

Following that initial discussion, where we were seduced with prospective returns in between 7% and 12%, we started a quest to figure out a lot more concerning these financial investment vehicles and the associated dangers. Not a lot is recognized concerning Mortgage Investment Corporations (MICs) owing to the truth that the huge bulk of MICs are normally exclusive firms.

Some Known Details About Mortgage Investment Corporation

In July 2000, Mr (Mortgage Investment Corporation). Shewan was chosen to the Realty Council of British Columbia. He offered as vice chair and chair in 2005 and 2006 specifically. The Property Council controls the licensing, education and learning and technique of actual estate licencees under the Realty Provider Substitute the District of British Columbia

MICs are comparable to various other companies in that they elect supervisors and police officers, assign boards, hire employees, and issue shares. Generally, a MIC will certainly accredit and provide several different courses of shares including common ballot shares and liked non-voting shares.

Mortgage Investment Corporation - The Facts

The MIC itself pays no revenue tax as the earnings are flowed with to the investors and strained at their hands. This is beneficial to a capitalist who has actually purchased M.I.C. shares with a self routed authorized retired life savings strategy (RRSP) or a self directed authorized retired life earnings fund (RRIF), as the tax obligation is delayed till the funds are redeemed or annuitized.

People and other navigate here companies are generally qualified to acquire M.I.C. shares; however, all M.I.C. reward payments are considered passion income for tax objectives. Essentially, a M.I.C. is like a home loan common fund. Q: Mr Shewan, why don't you tell us a bit concerning your firm, V.W.R. Resources? What are V.W.R.

VWR has around $90 million purchased private home loans of which, about 70 percent are first home loans. Over the following 3 years, the profile will grow depending on the demand for personal home loans. Currently VWR is preparing to enter the market in Manitoba on a traditional basis. Q: What is the difference between a Mortgage Investment Company (MIC) and an openly traded Realty Investment company site here (REIT)? A: A MIC invests primarily in mortgages as required under the legislation in the Income Tax Act.

The 10-Minute Rule for Mortgage Investment Corporation

Q: Are MIC's, generally, and shares in V.W.R. Resources's financial investment car, RRSP and TFSA eligible? Can they additionally be held in non-registered accounts? Exist any type of conditions to purchasing MIC's, that is, does one have to be a certified investor or exists a minimal financial investment etc? A: MIC's are qualified RRSP, RRIF, TFSA and RESP investments.